Decision Fatigue: Why Your Brain Shuts Down by Evening

In short: Debt stress is not only about numbers. It’s the ongoing strain of an unresolved obligation that the brain keeps treating as “not safe yet.” Even when nothing is happening in the moment, the future payment sits in the nervous system like an open loop—quiet, persistent, and hard to fully ignore.

Debt stress is not only about numbers. It’s the ongoing strain of an unresolved obligation that the brain keeps treating as “not safe yet.” Even when nothing is happening in the moment, the future payment sits in the nervous system like an open loop—quiet, persistent, and hard to fully ignore.

Why can debt feel so mentally loud, even on an ordinary day?

Because the mind is built to track unfinished commitments that could affect safety, shelter, status, and access to resources. When closure is delayed, the system stays partially mobilized, and everyday decisions start to carry extra weight.

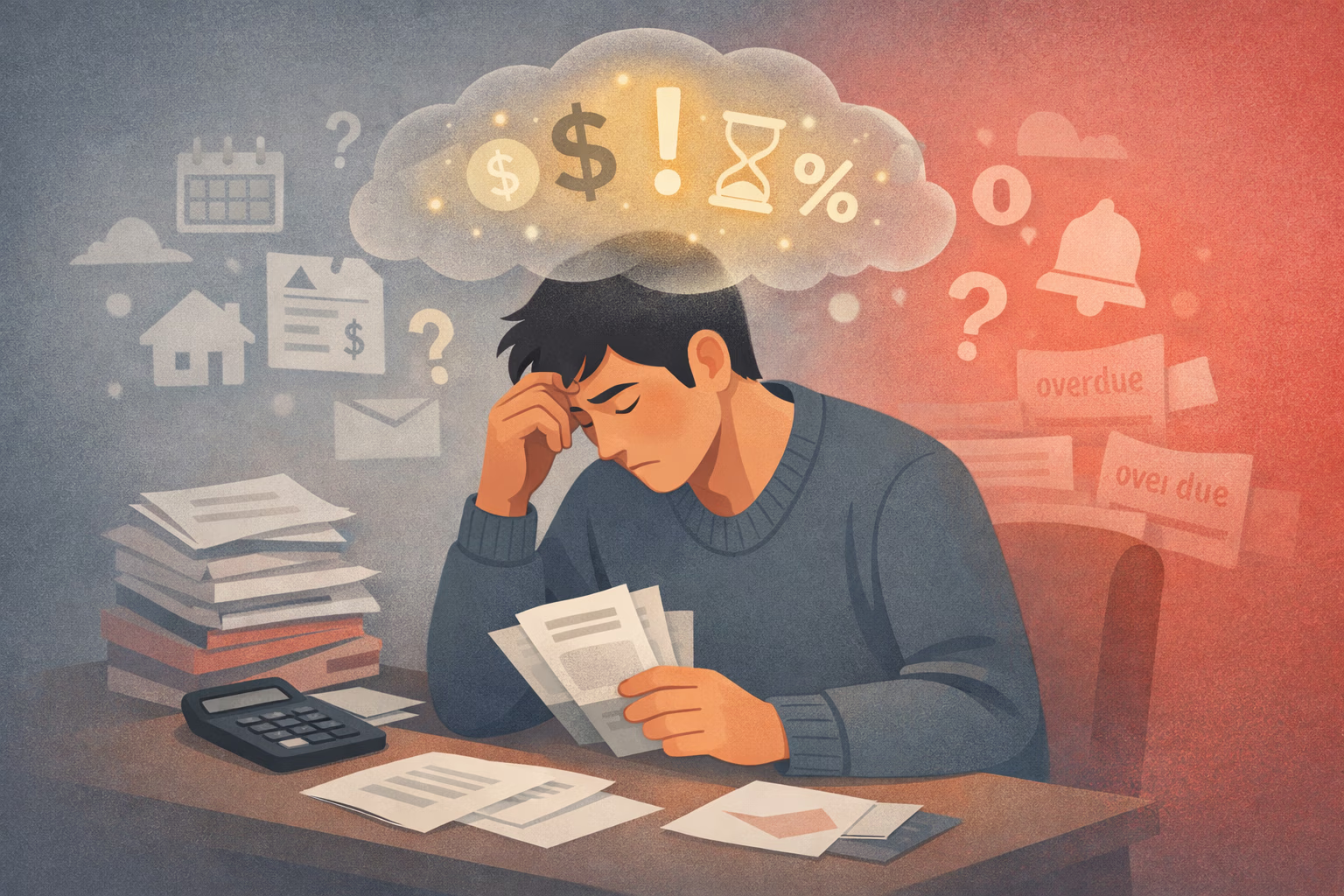

Many people describe debt stress as a constant background pressure: you can laugh with friends, go to work, make dinner—and still feel like you can’t fully relax. It can feel like living with a tab open in the mind that won’t stop refreshing.

This isn’t a lack of gratitude or resilience. It’s what happens when an obligation hovers behind every choice, quietly shaping what feels possible. The nervous system reads “unresolved” as “still relevant,” so it keeps scanning, budgeting attention, and holding tension in reserve. [Ref-1]

It’s not always panic. Sometimes it’s just never getting the “all clear.”

Threat and uncertainty take up working memory—the limited mental space used for planning, problem-solving, and flexible thinking. When debt is present, the brain often allocates resources to monitoring risk: calculating, anticipating, rehearsing outcomes, and bracing for surprises.

Over time, this can resemble a chronic stress state: elevated physiological arousal, more reactive attention, and fewer spare resources for creativity or long-range planning. In research, reducing debt has been associated with improved psychological functioning and shifts in decision-making—suggesting that load itself is a major driver of how we think and choose. [Ref-2]

Human threat systems evolved around immediate dangers and near-term resource loss: scarcity, social risk, shelter instability, and the consequences of falling behind. Debt is a modern form of ongoing obligation that can mimic those older conditions—especially when it touches housing, healthcare, family stability, or basic security.

Because the system is tuned for survival relevance, it doesn’t file debt away as “just paperwork.” It tracks it as an unresolved claim on future resources. That is why the stress can persist even when you’re doing everything you can: the loop is not complete, so the signal doesn’t fully stand down. [Ref-3]

What if your mind isn’t broken—just stuck managing an unfinished safety task?

Under sustained load, the nervous system looks for ways to reduce immediate strain. Two common regulatory responses can look opposite on the surface:

Both can reduce activation in the short run by changing what the mind has to hold at once. Avoidance creates distance from the signal; overcontrol reduces uncertainty by compressing life into a solvable problem. Neither response is an identity—both are attempts to regulate overload when closure feels out of reach. [Ref-4]

It can be tempting to believe that not looking protects you. And in the moment, it sometimes does—because attention is one of the fastest ways to change state. But the nervous system is still tracking the unresolved obligation, even if the conscious mind is trying to put it away.

That’s why “not thinking about it” often doesn’t restore clarity. The load stays in the background, quietly draining energy and making ordinary tasks feel heavier than they should. Many people experiencing debt also report impacts on mental well-being, suggesting the strain is not only financial but cognitive and physiological. [Ref-5]

Debt stress often forms a self-reinforcing pattern—not because people “won’t deal with it,” but because high load changes what the brain can do. When threat activation is high, attention narrows. When attention narrows, flexible planning becomes harder. When planning is harder, the path to closure feels more complex, and the system stays activated.

This is an Avoidance Loop: the obligation increases cognitive strain; the strain reduces bandwidth; reduced bandwidth delays resolution; the continued lack of closure keeps the obligation feeling urgent and ever-present. Research linking changes in debt status with changes in psychological functioning supports the idea that load and decision capacity move together. [Ref-6]

In high load, the mind doesn’t become “lazy.” It becomes protective—and protective systems prefer short-term relief.

Debt stress can show up in ways that don’t look “financial” at all. These patterns often reflect a system carrying too many open loops at once, not a lack of character.

Notice how many of these are about bandwidth, attention, and capacity—not about moral strength. They are the shape a nervous system takes when it is trying to stay functional under ongoing threat signals.

Prolonged debt stress can quietly distort time. The mind becomes oriented around the next bill, the next penalty, the next unknown. Long-term goals may feel abstract or even unsafe to imagine, not because you don’t care, but because the nervous system is prioritizing immediate containment.

Over time, this can affect health, mood stability, problem-solving, and a person’s sense of self-efficacy—especially when debt intersects with broader socioeconomic pressure. Public health sources have documented associations between household debt and health impacts, reinforcing that this is a real load with real bodily consequences. [Ref-8]

When the system is busy preventing loss, how much space is left for building a life?

Planning requires spare capacity: the ability to hold options, evaluate tradeoffs, and tolerate uncertainty long enough to choose. Debt stress reduces that spare capacity, which can delay the very steps that would create resolution. This is how the sense of being trapped can intensify even when a person is actively trying.

Studies suggest that as debt burden changes, decision-making and psychological functioning can shift too—consistent with the idea that reducing load restores mental room for more future-oriented choices. [Ref-9]

Sometimes the hardest part isn’t the math—it’s doing the math while your brain is bracing.

There’s a specific kind of internal shift that can happen when the debt is no longer a vague cloud but a recognized, bounded reality: the scanning slows. Not because everything is solved, and not because insight magically heals—but because uncertainty often costs more than difficult certainty.

When the obligation becomes legible, the nervous system can allocate attention more efficiently. Mental space can begin to return in small pockets: less background checking, fewer sudden spikes of dread, more moments of “I’m here” rather than “I’m behind.” This is not optimism; it’s a reduction in load that allows a more stable baseline. [Ref-10]

What changes when debt is no longer a verdict, but a defined situation?

Debt often becomes private—not necessarily by choice, but because money is socially charged. When the burden is carried alone, the mind has to do everything: remember, forecast, brace, and self-regulate in isolation. That solitary load can intensify shame and make the problem feel bigger than the person.

When planning becomes shared—through transparency, trusted support, or simply not being alone with the mental math—the cognitive burden distributes. The situation can start to feel more workable because it’s no longer held entirely inside one nervous system. Connections between mental health and financial health are well documented, including how stress and isolation can amplify each other. [Ref-11]

When debt-related threat signals reduce—whether through progress, stabilization, or increased predictability—people often notice changes that are more physiological than motivational. The mind stops snapping back to the same worry track. Decisions require less effort. The day holds more space.

Research on changes in debt burden has observed improvements in psychological functioning and decision-making, consistent with the idea that reduced financial threat load supports clearer thinking. [Ref-12]

One of the most painful effects of debt stress is identity collapse: “I am my balance,” “I am behind,” “I am irresponsible.” But debt is a condition, not a self. Under high load, the brain tends to compress complex lives into a single organizing threat, because simplicity is easier to manage than nuance.

As clarity and capacity return, the story can widen. Debt becomes part of a larger plan—connected to real-life contexts like caregiving, education, medical costs, job disruption, migration, or simple survival in an expensive world. When threat activation softens, people often regain future orientation and a more integrated sense of agency, even before the numbers are fully resolved. [Ref-13]

Meaning returns when life stops being only about containment.

Debt stress makes sense in a nervous system designed to track unresolved obligations. If you feel scattered, avoidant, or overly controlling, that may be your system protecting you from relentless cognitive strain—not evidence that you’re “bad with money.”

In many communities, debt is common, structural, and tied to unequal costs of living and access to stability. Naming debt stress as a real cognitive load can reduce shame and restore dignity: this is something you’re carrying, not something you are. And when dignity is present, the mind has a better chance of returning to coherence—where choices can align with values, relationships, and the life you’re trying to hold together. [Ref-14]

Numbers matter. But so does what happens inside the person living with them. When cognitive load lightens, even slightly, the world often becomes more navigable: fewer threat alarms, more usable attention, and a steadier sense of direction.

That steadiness is not denial, and it isn’t a motivational speech. It’s what can emerge when the nervous system gets more closure and less constant scanning. Meaning can return before the balance hits zero—because coherence is the beginning of movement, and clarity is often the first sign that the system is no longer trapped in pure survival mode. [Ref-15]

From theory to practice — meaning forms when insight meets action.

Because the nervous system tracks unresolved obligations whether or not the conscious mind is looking at them. Debt sits in the body as an open loop the Threat & Safety System reads as 'still relevant,' so it keeps scanning, budgeting attention, and holding tension in reserve. That uses working memory — the same limited mental space needed for planning, problem-solving, and flexible thinking — which is why even ordinary days can feel heavy. It isn't a lack of resilience or gratitude; it's what happens when an obligation hovers behind every choice and the system never quite gets the all-clear signal to stand down.

Only on the surface, and only briefly. Attention is one of the fastest ways to change state, so not looking can produce real momentary quiet. But the nervous system is still tracking the unresolved obligation in the background, which is why 'not thinking about it' rarely restores clarity — the load keeps draining energy and making ordinary tasks feel heavier than they should. The article frames both avoidance (postponing bills) and overcontrol (hyper-focusing on budgets) as legitimate regulatory responses to overload, neither of which is identity. They're attempts to reduce immediate strain when closure feels out of reach.

Because planning requires spare cognitive capacity — holding options, evaluating tradeoffs, tolerating uncertainty long enough to choose — and debt stress reduces that spare capacity. High threat activation narrows attention, narrowed attention makes flexible planning harder, harder planning delays resolution, and continued lack of resolution keeps the obligation feeling urgent. That's the Avoidance Loop: load reducing bandwidth, and reduced bandwidth deepening load. The trapped feeling can intensify even when a person is actively trying. The hardest part often isn't the math; it's doing the math while the body is bracing. Reducing the load is what restores the room to plan.

Yes, and the article is specific about why. Uncertainty often costs the system more than difficult certainty does. When debt becomes a recognized, bounded reality rather than a vague cloud, the nervous system can stop scanning and allocate attention more efficiently. People notice less background checking, fewer sudden spikes of dread, more moments of 'I'm here' rather than 'I'm behind.' This isn't optimism or denial — it's a structural reduction in load that allows a more stable baseline to return. Debt becomes a chapter rather than an identity, which is the beginning of agency, even before the numbers fully resolve.

From Science to Art.

Understanding explains what is happening. Art allows you to feel it—without fixing, judging, or naming. Pause here. Let the images work quietly. Sometimes meaning settles before words do.

One Quiet Window, one insight, one reflection — every Sunday