Avoidance Loops: Why You Delay What You Care About

In short: For many people, “being on top of money” doesn’t fail because of laziness or lack of caring. It fails because certain financial cues—an envelope in the mail, a low-balance notification, a login screen—land in the body as threat.

For many people, “being on top of money” doesn’t fail because of laziness or lack of caring. It fails because certain financial cues—an envelope in the mail, a low-balance notification, a login screen—land in the body as threat. When that happens, the nervous system may shift into shutdown: not deciding, not opening, not looking.

What if procrastination around money isn’t a motivation problem—but a safety response?

Financial avoidance is often a form of self-protection under load. It can create a brief sense of quiet by removing a threat cue from awareness, even while the unfinished reality continues running in the background. Understanding that structure can reduce shame and make the pattern feel more orienting: something that happens in certain conditions, not something you “are.”

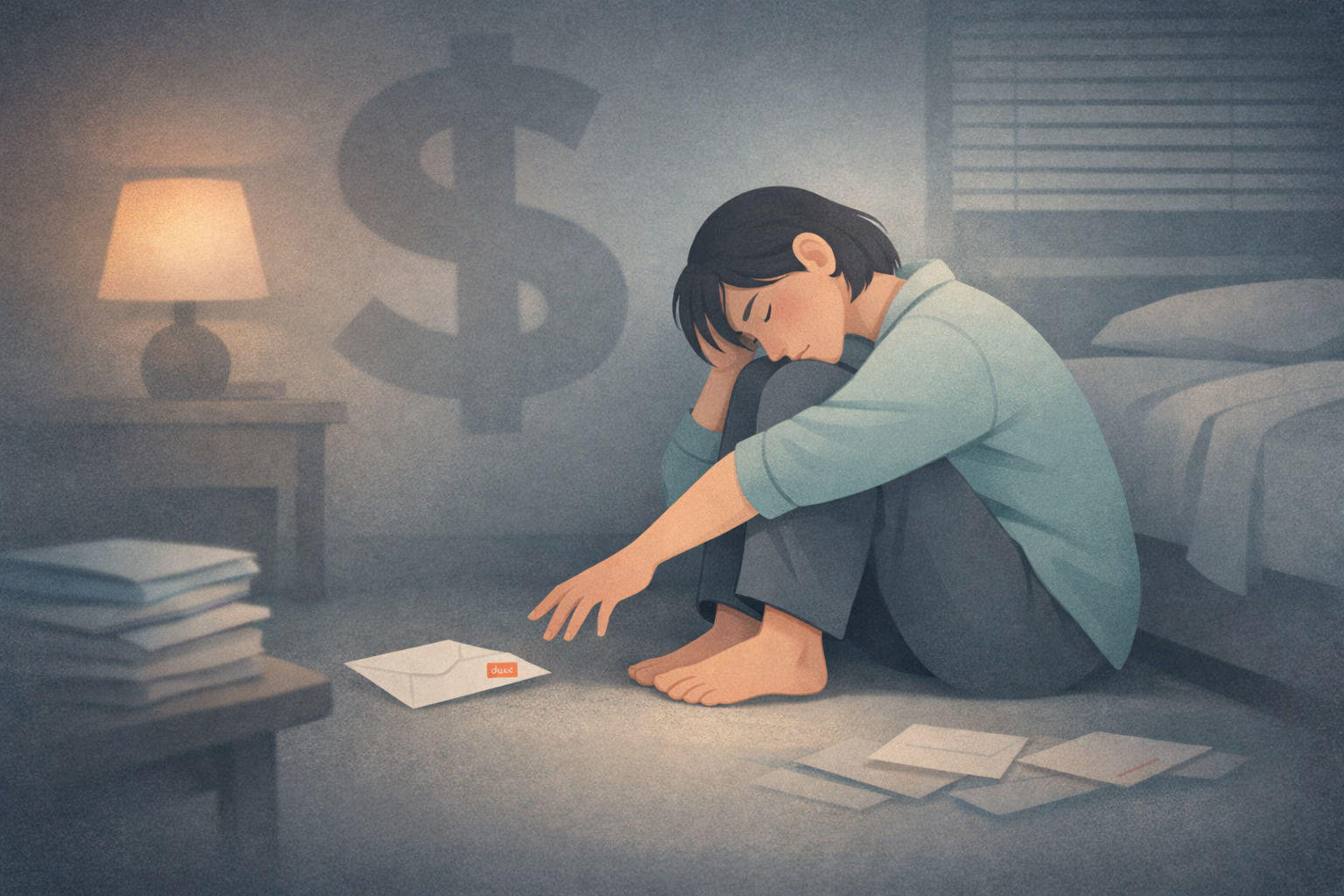

People often describe a specific kind of dread around money tasks: opening bills, checking balances, reading a message from a provider, logging into a banking app. It can feel like the task itself is heavy—yet the weight is frequently the bodily response that arrives before any numbers appear.

In the moment, avoidance can bring quick relief: the envelope stays closed, the notification is swiped away, the tab is closed. But the nervous system doesn’t register “done.” It registers “unresolved.” So the relief is often paired with a quieter, ongoing hum of vigilance—like carrying a backpack you can’t set down. [Ref-1]

When finances feel unsafe, the brain and body can shift into a protective mode that prioritizes immediate survival signals over long-horizon thinking. This is not a moral issue. It’s what threat physiology does: it reallocates resources away from flexible planning, sequencing, and working memory.

That’s why a task that looks “small” on paper—find the statement, open the email, make one call—can feel strangely impossible. The system isn’t refusing effort; it’s reducing exposure. In a narrowed state, ambiguity becomes louder, and decisions can feel high-stakes even when they’re ordinary. [Ref-2]

Freeze and shutdown are not new. In nature, when escape is unclear or a threat feels inescapable, immobility can be protective. It reduces detection, reduces energy use, and buys time while the organism searches for safety signals.

Financial stress can mimic that “inescapable threat” profile, even though it’s abstract. A bill isn’t a predator—but it can represent consequences, uncertainty, status risk, or past experiences of scarcity. So the body responds as if the safest move is to become still: don’t look, don’t touch, don’t engage. In modern life, though, money problems resolve through contact and completion, not immobility—creating a painful mismatch between what the nervous system selects and what the situation requires. [Ref-3]

Avoidance is often misunderstood as “not caring.” More accurately, it’s a fast method for lowering intensity. If the cue is the trigger, removing the cue can bring the system down a notch—at least temporarily.

This is why financial avoidance can be so sticky: it’s negatively reinforcing. The brain learns, “When I don’t open the bill, my body feels calmer.” The calm is real, but it’s state-change calm, not completion-calm. The underlying loop stays unfinished, so the nervous system remains partially mobilized in the background. [Ref-4]

Avoidance can create the illusion that stress is reduced. But unaddressed money tasks tend to grow: late fees accumulate, timelines narrow, letters sound more urgent, and options can feel fewer. Over time, the environment itself becomes more threatening—not because you “failed,” but because unresolved systems naturally compound.

Meanwhile, shame often appears as a secondary load. Not as a cause, but as an extra layer of pressure that rides on top of the original threat. The result is a widening gap between “what needs attention” and “what feels possible,” which makes the trigger stronger the next time it appears. [Ref-5]

Financial avoidance often follows a predictable loop:

This is how a nervous system can become trained into freezing around money. The loop isn’t about poor character; it’s about the body learning a fast exit from overload, then meeting a world that keeps returning the problem with increased intensity. [Ref-6]

Because this is a regulatory pattern, it often appears as behaviors that look “irrational” from the outside but feel protective from the inside. Some common forms include:

It can feel like you’re not choosing avoidance. It can feel like your system simply goes offline.

These are not personality traits. They’re patterns that emerge when cues repeatedly arrive without enough capacity, clarity, or closure to complete the loop. [Ref-7]

When avoidance lasts, the impact is rarely limited to money. It can affect sleep, concentration, and social ease, because the nervous system carries an ongoing “open loop” signal. Even in quiet moments, the background knows something unresolved is waiting.

Over time, self-trust can erode—not as a moral failing, but as a predictable result of repeated non-completion. If your body has learned that money cues lead to shutdown, it makes sense to feel less confident about future engagement. And when finances worsen due to delays, the environment provides stronger threat cues, which further loads the system. This is how financial stress and anxiety can become mutually reinforcing. [Ref-8]

Learning doesn’t only happen through insight. It happens through repetition in the body. Each time a money cue triggers shutdown and the situation later returns with more urgency, the nervous system receives a simple lesson: exposure equals danger.

In that sense, avoidance is not merely “putting it off.” It’s conditioning. The association strengthens: bills → threat → disengagement. And because shutdown reduces sensation and narrows attention, it can also create gaps in memory and continuity—making it harder to build a stable, coherent “money narrative” that feels finished and reliable. [Ref-9]

There’s an important difference between forcing engagement and becoming able to engage. When threat softens—even slightly—the mind can make tolerable contact with financial reality without immediately tipping into overwhelm. That shift is less about courage-as-effort and more about safety-as-capacity.

This is where change often begins, not as a dramatic breakthrough, but as a quieter reorganization: the body can stay present long enough for a small piece of reality to be processed. Not just understood, but metabolized—registered as something you can touch and survive. Over time, those completed contacts can create a new expectation: “This can be handled.” [Ref-10]

Money avoidance tends to be private. Privacy can protect dignity in the short term, but isolation can intensify threat in the long term—because the nervous system reads isolation as “no backup.”

In contrast, a non-judgmental conversation or shared accountability can change the safety math. When another person can hold context without punishment or pressure, the task becomes less like solitary exposure and more like supported contact with reality. The goal isn’t confession; it’s reducing the load of secrecy and making engagement feel less dangerous. [Ref-11]

As engagement becomes more manageable, people often notice a specific kind of relief: not the buzz of motivation, but the quiet of fewer open loops. Clarity increases because the mind is no longer spending so much energy guarding against reminders. Agency increases because choices feel available again.

Importantly, this relief is often proportional to completion, not to insight. You can understand your pattern for years and still feel frozen—until enough threat has softened and enough small loops have actually closed that your system starts to stand down. That’s when steadier sleep, improved focus, and a more stable baseline can become more realistic. [Ref-12]

Money tasks often get framed as performance: proof of adulthood, intelligence, or worth. Under that frame, each bill becomes a verdict. It makes sense that the system would shut down.

But money can also be framed as structure: a way to support housing stability, reduce future stress load, protect health, or create room for what matters. When re-engagement is gentle enough to be tolerable, those tasks can start to land as life-supporting rather than identity-threatening. In time, “checking” and “paying” can become less of a danger signal and more of a closure signal—an endpoint the body can recognize. [Ref-13]

If bills trigger shutdown for you, it may help to name what’s happening accurately: a protective response to overwhelm, not a personal defect. The pattern often formed in conditions where the system needed a fast reduction in intensity and didn’t have enough capacity or support to complete what was in front of it.

When you view financial avoidance as a nervous-system strategy—imperfect but understandable—self-blame tends to lose some grip. And when blame loosens, there is often more room for pacing, dignity, and realistic contact with reality to re-enter the picture. Not as an instruction, but as a shift in what feels possible. [Ref-14]

Facing money slowly still counts as facing money. The nervous system doesn’t build stability through force; it builds stability through experiences that reach completion without overwhelming the system.

Over time, repeated moments of tolerable contact can change what your body expects from financial reality. Less alarm, more continuity. Not because you became a different person, but because your environment and your load finally allowed closure to do its quiet work. [Ref-15]

From theory to practice — meaning forms when insight meets action.

Because for many nervous systems, money cues — an envelope, a low-balance notification, a login screen — land as threat cues. The dread you feel before any numbers appear is the body's response to anticipated danger, not laziness. When threat is perceived, the brain shifts into protective mode that prioritizes immediate survival signals over long-horizon thinking. A task that looks small on paper becomes strangely impossible because the system isn't refusing effort; it's reducing exposure. Procrastination around money isn't a motivation problem — it's a safety response. Threat & Safety physiology selecting freeze when escape feels unclear.

Because removing the cue removes the trigger, which lowers intensity. The brain learns: when I don't open the bill, my body feels calmer. The calm is real — but it's state-change calm, not completion-calm. The nervous system doesn't register done; it registers unresolved. So relief is paired with a quieter, ongoing hum of vigilance — like carrying a backpack you can't set down. Meanwhile, late fees accumulate, timelines narrow, and shame appears as a secondary load. The Avoidance Loop tightens: shutdown increases consequence, consequence increases the next round of shutdown.

Because freeze and shutdown are ancient responses for situations where escape feels unclear or threat feels inescapable. Immobility reduces detection and energy use. Financial stress can mimic this inescapable threat profile even though it's abstract — a bill represents consequences, uncertainty, status risk, or past scarcity. The body responds as if the safest move is to become still: don't look, don't touch, don't engage. The painful mismatch is that money problems resolve through contact and completion, not immobility. The blankness isn't your intelligence failing; it's your nervous system selecting an old protective pattern.

Through tolerable contact, not forced courage. There's an important difference between forcing engagement and becoming able to engage. When threat softens — even slightly — the mind can make contact with financial reality without immediately tipping into overwhelm. The body needs to stay present long enough for a small piece of reality to be processed and metabolized, not just understood. Each completed contact creates new expectations: this can be handled. Support helps because isolation reads as no backup. The nervous system doesn't build stability through force; it builds stability through experiences that reach completion without overwhelming it.

From Science to Art.

Understanding explains what is happening. Art allows you to feel it—without fixing, judging, or naming. Pause here. Let the images work quietly. Sometimes meaning settles before words do.

One Quiet Window, one insight, one reflection — every Sunday